AUD

AUD

Loading... Please wait...

Loading... Please wait...

Recent Posts

TICK TOCK! Count Down to Economic Armageddon Officially Begins

Posted by on

The official countdown to Economic Armageddon has now begun.

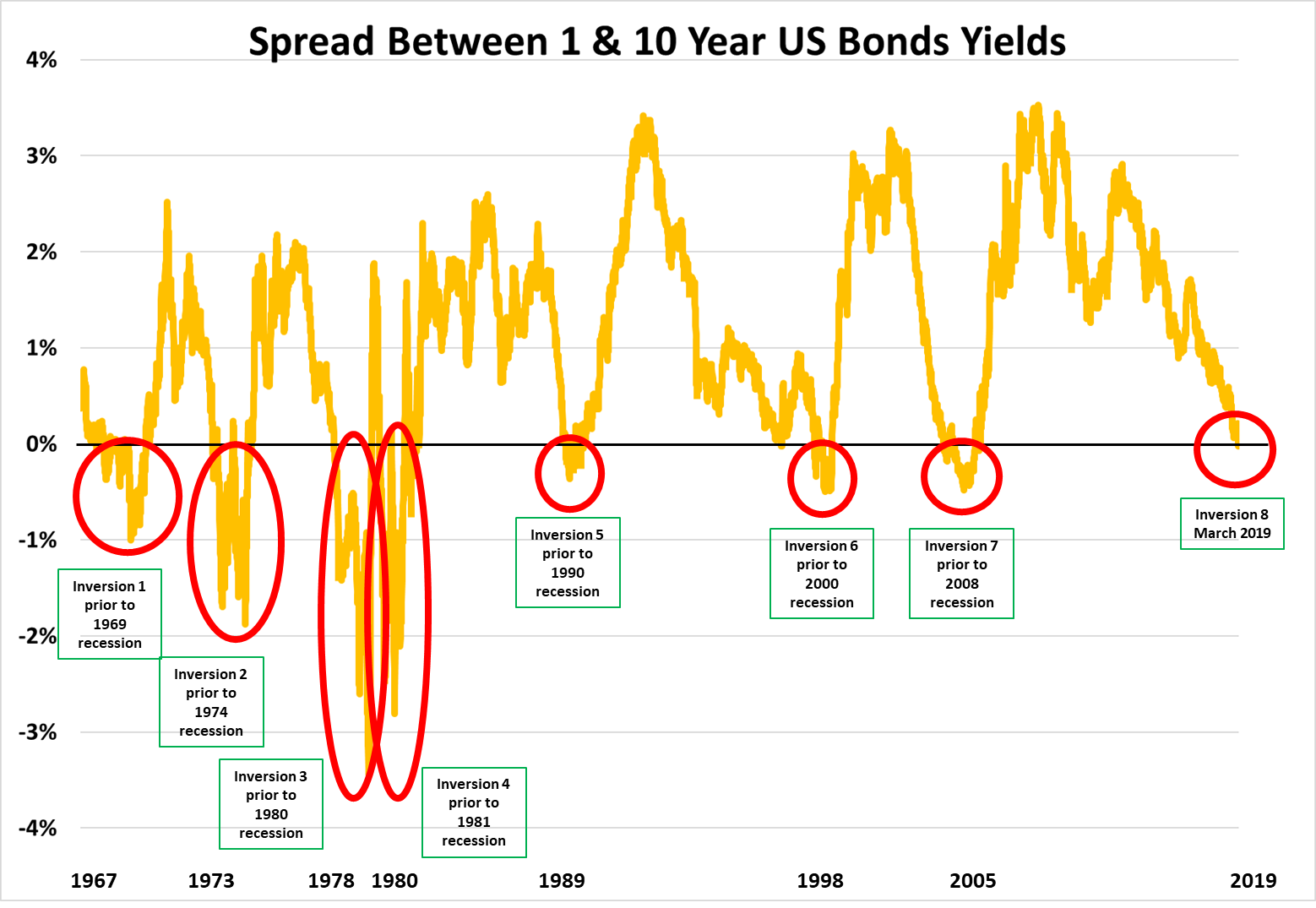

In the past 24 hours, the most accurate signal of a US economic recession (i.e. two or more quarters of negative economic growth) has manifested itself in the US Bond market - that being an inversion of the ‘1-year to 10-year’ yield curve.

An inversion of the yield curve is generally an unusual economic occurrence and signifies that:

- market confidence in short term US economic conditions has become bearish; and

- monetary policy settings (i.e. short-term interest rate policy) are too restrictive (i.e. short‑term interest rates being too high) at the same time that economic growth is slowing.

Mathematically, a yield curve inversion means that the interest rate (or yield) on 1-year US Government treasury bonds is higher than the interest rate on 10-year Government treasury bonds.

This technically means that market demand for short-term bonds has fallen, while demand for longer-term bonds has risen thus making it more difficult for banks and other financial institutions to lend more profitably resulting in a credit squeeze.

This occurrence is opposite to what typically happens in a healthy economy, where government and corporate bonds that have longer maturity periods pay investors higher interest rates.

Specifically, as of 23 March 2019 [1], the yield on 1-year US Government bonds reached 2.454%, while the yield on 10 year government bonds reached 2.435% representing an inverted ‘1 year to 10 year’ yield spread of -0.019%.

- The significance of the US Government bond market yield curve as a future barometer of US economic conditions has long been recognised by American and International market observers and has become a subject of interest for economic researchers, including at the US Federal Reserve.

A 2018 research note from the Federal Reserve Bank of San Francisco’s officials Michael Bauer and Thomas Mertens, titled “Economic Forecasts with the Yield Curve” [2] stated:

“Every recession over this period (January 1955 – February 2018) was preceded by an inversion of the (1 - 10 year) yield curve, that is, an episode with a negative term spread.”

Over this period, 1955 – 2018, an inversion of the ‘1-year to 10-year’ yield curve has occurred prior to nine economic recessions and has only produced one false positive reading that being in September 1965, where an inversion of the yield curve proceeded an economic slowdown (economic growth only grew by 0.06% in the 2 nd quarter of 1967) but not an official economic recession.

An economic recession has not occurred in the United States over the past 50 years without a preceding inversion of the ‘1-year to 10-year’ yield curve occurring.

From a timing perspective, an inversion of the ‘1-year to 10-year’ yield has signalled, across the last 7 recessions dating from 1969 – 2019 (see Graph 1 below), that an economic recession (i.e. two or more quarters of negative economic growth) in the United States will commence between 3 ‑ 27 months after the inversion as shown in Table 1 below.

Graph 1: Inversion of the 1 Year – 10 Year Bond Yield

Table 1: Time lag between Yield Curve Inversion and Economic Recession

| No | US Economic Recession | Date of Inversion | 1st Quarter of Negative Economic Growth | Time between Inversion and 1st Quarter of Negative Economic Growth |

| 1 | Economic Recession of 1969 | 06/12/1967 | 4 th Quarter 1969 | 21 months |

| 2 | Economic Recession of 1973-74 | 09/03/1973 | 3 rd Quarter 1973 | 3 months |

| 3 | Economic Recession of 1980 | 18/08/1978 | 2 nd Quarter 1980 | 19 months |

| 4 | Economic Recession of 1981 | 15/09/1980 | 2 nd Quarter 1981 | 6 months |

| 5 | Economic Recession of 1990 | 25/01/1989 | 4 th Quarter 1990 | 20 months |

| 6 |

Economic Recession of 2001

(Dot Com Crash) |

21/09/1998 | 1 st Quarter 2001 | 27 months |

| 7 | 2008 Global Financial Crisis | 27/12/2005 | 1 st Quarter 2008 | 24 months |

Importantly. the occurrence of an inverted yield curve in the United States not only has direct implications for the US economy, but carries implications for the global economy given that the US economy is still the largest in the world.

A US economy that is headed towards recession is likely to have material implications for world financial markets and the global economy, especially given that:

- the US is still the centre of the world’s financial system and has some of the largest Global Systemically Important Banks;

- the US Government and US corporations have a historically high level of debt relative to US Gross Domestic Product;

- an economic recession will impact US fiscal and monetary policy, including US interest rates as well as the international liquidity and value of the US dollar; and

- the global economy has the largest amount of debt ever which stands in excess of $US 250 trillion and a slow down in global economic growth will severely impact the ability of nations around the world (especially China) to service their debts irrespective if these debts are held among governments, corporations or households.

Implications for Australia

With the largest economy in the world and the centre of world financial markets now on track towards an economic recession, there can be no question that Australia will be impacted. The outstanding issue is by what degree.

A lot will depend on the policy decisions made by governments and central banks both in Australia and around the world as well as the timing and sequence of these decisions.

For example, if policy makers continue to implement contractionary macroeconomic policies whether they be of a monetary (including quantitative tightening), macroprudential or fiscal nature, the US and global economies could reach a point where either higher interest costs, collapsing credit growth or a lack of financial liquidity could make global debts unserviceable resulting in:

- a series of defaults and debt restructures[3];

- a collapse in economic confidence among consumers and businesses; and

- economic contagion that involves global systemically important institutions which in turn engulfs entire global industries and multiple economies.

Alternatively, US and global policy makers, knowing that the US economy is on track for a recession, could start to implement pre-emptive fiscal and monetary stimulus measures such as lowering interest rates, ending quantitative tightening, re‑instituting quantitative easing, introducing Universal Basic Income (based on exotic theorems such as Modern Monetary Theory) or providing fiscal incentives to defend and protect the global debt bubble in order to soften the economic slowdown and/or official recession.

In either scenario, the policy prescriptions as outlined above is likely to have either a profound deflationary (if global debts become unserviceable) or inflationary (if pre-emptive stimulus is implemented) impact on the Australian economy that will materially affect living standards.

It is very likely that Australians who either:

- are struggling with debt and/or hold overvalued assets (in the deflationary case); or

- have little real wealth, live in urbanised cities, hold Australian dollars, have fixed incomes and rely on selling their labour for income (in the inflationary case)

will face significant economic adversity, especially if they have not taken any preparatory steps before global economic events begin to intensify.

Now that the clock towards Economic Armageddon has now officially started, Australians, who are awake, will be rushing towards the exit doors before it is too late.

Australians still do have time to financially and psychologically prepare themselves, but the window to do so is closing fast.

[1] The yield curve inverted on the morning of Saturday 23 March 2019, Australia EST. In US terms, the yield curve inverted during the trading session of Friday, 22 March 2019.

[3] Historically, major defaults on debt typically represent a major economic shock or disruption.